ইন্টারনাল অডিট স্কিম সম্পর্কিত তথ্য

SCHEME ON INTERNAL AUDIT AND ADUIT FOLLOW-UP

Strengthening Public Financial Management Program to Enable Service Delivery (SPFMS)

Finance Division, Ministry of Finance

Introduction

Internal Audit Scheme was initially planned to start in 2018 but due to some dispute regarding implementation rotation either in the Ministries or in the Departments, it was delayed, and also the Covid pandemic situation has affected the progress of this scheme. It’s been a challenge in Bangladesh, to introduce an Internal Audit. If look back in 2009, there is Public Money and Budget Management Act; it states that one of the duties and responsibilities of the Principal Accounting Officer (PAO) shall be “To ensure efficient and transparent financial management and internal control processes at the relevant Ministry or Division or Other Institution”. Internal audit will assume responsibility for periodically evaluating internal control operations to identify weaknesses and recommend corrective measures. This general mandate for the establishment of the internal audit was communicated through more specific instructions from the Finance Division’s memo No. MF\FD\B-1\budget (04) \2005\1803 dated 22\08\05. However, a formal internal audit function has not been established. Only a few Ministries have an IA function, and these are not adequately staffed with qualified auditors. The IA manual that was developed under the Strengthening Public Expenditure Management Program has not been effectively used. Even the 2015 PEFA Report identified weaknesses within the IA function.

Finally, under the Strengthen Public Financial Management to Enable Service Deliver (SPFMS) program Finance Division has agreed to include IA functions in the public sector as part of the PFM reform because internal auditing primarily provides an independent objective opinion to the Head of the Government Department/ Office. The findings of an independent focused internal audit function also bring to the fore its findings and recommendations which act as a tool to officers in a department to take suitable corrective action and help in plugging the loopholes which would otherwise go undetected for a considerable period of time.

The Internal Audit (IA) scheme start date is September 2021 and closing date is June,2023.

Objective

A PFM Action Plan (2018-23) has been approved in September 2018 to support effective implementation of the PFM Reform Strategy (2016-21). The strategic goals of PFM reforms are to:

- Maintain aggregate fiscal discipline compatible with macro-economic stability and pro-poor growth;

- Allocate resources consistent with Government priorities as reflected in National Plan;

- Promote the efficient use of public resources and delivery of services through better budget execution;

- Promote accountability through external scrutiny and transparency of the budget; and

- Enhance the enabling environment for improved PFM outcomes.

Within these goals, the PFM Action Plan provides the implementation roadmap for some priority actions with clear institutional responsibilities among 13 thematic reform components, cost-benefit analysis of sub-activities, and results indicators to monitor the successful implementation. Component-10 of PFM Action Plan is Financial Reporting under which Internal Audit & Audit Follow-up scheme is expected to play an important monitoring role in evaluating the effectiveness of the control systems within the Government’s operations in meeting its strategic objectives. There is some improvement in adherence to systems of control in contrast to the recent past, although, a lot more needs to be done to strengthen the overall systems of internal control.

The Internal audit function when established should play an important monitoring role in evaluating the effectiveness of the control systems within the Government’s operations in meeting its strategic objectives. To discharge its functions effectively, the internal audit unit must possess the key twin attributes of (i) professionalism - audit practice should be in accordance with International Standards for the Professional Practice in Internal Audit (ISPPIA) issued by the Institute of Internal Auditors (IIA); and (ii) independence - not involved in maintaining the controls it is supposed to evaluate. The overall objective of the scheme are as follows:

- To establish a modern internal audit function in selected large spending and high-risk departments as part of internal controls using risk-based audit methods concentrating on systemic issues and providing independent and objective advice to management;

- To establish a system for carrying out annual procurement post reviews and follow up of actions recommended for improving procurement and contract management.

Goal

- An Independent, objective assurance and consulting activity designed to add value and improve an organization’s operations.

Disbursement Link Indicators & Results

SPFMS program is comprised with 10 Disbursement Link Indicators (DLIs) and under 10 DLIs there are 45 Disbursement Link Results (DLRs). DLI 9 is responsible for this Internal Audit and Audit Follow-up Scheme. DLI 9 state that:

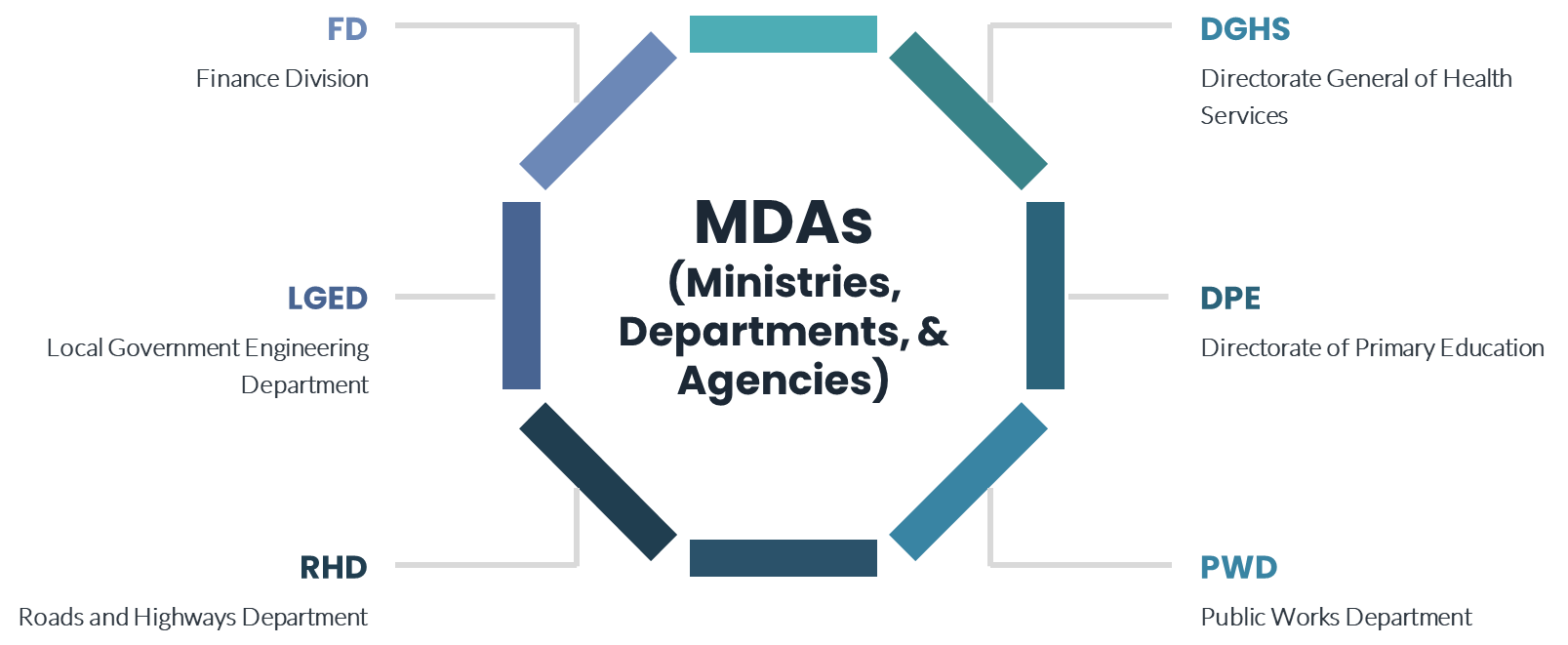

DLI 9: Action taken on internal and external audit reports in selected MDAs - (finance division, education, health, roads, public works, & local government) and procurement for FD.

DLI 9: Action taken on internal and external audit reports in selected MDAs - (finance division, education, health, roads, public works, & local government) and procurement for FD.

Under DLI 9 the following DLRs needed to be achieved throughout the span of this program:

|

DLRs/ Targeted outcome |

|

DLR 9.1: The Model Internal Audit Charter and the Risk-based Internal Audit Manual have been issued by the Finance Division. |

|

DLR 9.2: A system for annual procurement planning and post-review has been established by the Finance Division and training on the system has been conducted. |

|

DLR 9.3: Internal audit reports, prepared in accordance with the Model Internal Audit Charter and the Risk-based Internal Audit Manual issued under DLR 9.1, have been issued to the heads of departments and principal accounting officers of any two departments in any of the Selected MDAs |

|

DLR 9.4: The relevant Audit Committees resolve 50% of: (i) audit recommendations for each of the Selected MDAs, other than the Finance Division and (ii) audit recommendations and procurement post-reviews in Finance Division, based on the stock of total audit recommendations and procurement post-reviews, as applicable, pending for each of the relevant Selected MDAs and the Finance Division respectively, at the beginning of the relevant Fiscal Year in which the DLR is being assessed. |

Program Governance Structure

The PFM reform program has a two-tier governance and coordination structure – comprising a Steering Committee (SC) and a Program Execution and Coordination Team (PECT). Such Governance and coordination structure of PFM reform is providing a mutual learning and accountability platform among the relevant institutions for sustained use of improved PFM procedures and systems. In close coordination of PECT, 13 PITs (Program Implementation Teams) formed in different PFM institutions, that have the primary accountability of implementing the respective PFM Action Plan components, preparing implementation documentation such as work plan and budget allocation, providing financial oversight on program implementation, and achieving the performance targets.

The following Governance Structure have been followed under this Scheme of Internal Audit and Audit Follow-up: